Good news for individuals

Good news for individuals

By Beatrie Gouws

The stronger fiscal outlook presented in the 2025 Medium Term Budget Policy Statement (MTBPS) meant that key metrics remain in line with the fiscal strategy. The tail winds of tax buoyancy, and tax system resilience, meant that Government could withdraw previously announced tax increases for the 2026 Budget and to provide inflationary relief to taxpayers.

We list a variety of positive changes affecting individuals below.

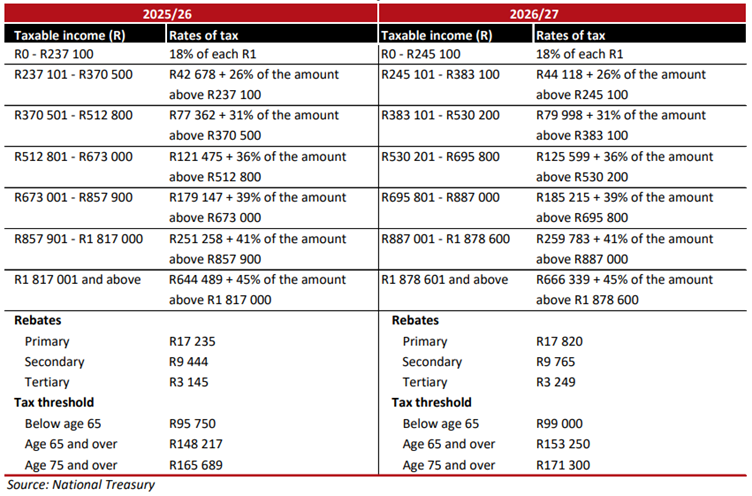

Inflationary adjustment to personal income tax brackets and rebates:

Inflationary adjustment to medical tax credits:

Medical tax credits will increase from R364 to R376 for the first two members, and from R246 to R254 for additional members.

Savings:

- The tax-free annual investment limit will be increased from R36 000 to R46 000 per year (last increased in 2021).

- The limit on retirement fund contribution deductions will be raised from R350 000 to R430 000 (last increased in 2016).

- The de minimis retirement interest threshold for annuitisation will be increased from R247 500 to R360 000 (last increased in 2016).

- The threshold for living annuity commutation will be increased from R125 000 to R150 000 (last increased in 2020).

Donations tax:

The exemption for donations made by individuals will be increased from R100 000 to R150 000 (last increased in 2007).

Tax exempt employment benefits affecting individuals:

- The annual remuneration ceiling in respect of bursaries and scholarships for all employees including persons with disabilities, will be raised from R600 000 to R900 000 (last amended in 2017).

- The annual ceiling for bursaries and scholarships in respect of employee relatives' primary / secondary education will be increased from R20 000 to R30 000 and from R30 000 to R45 000 for persons with disabilities (last amended in 2017).

- The annual ceiling for bursaries and scholarships in respect of employee relatives' tertiary education will be increased from R60 000 to R90 000 and from R90 000 to R130 000 for persons with disabilities (last amended in 2017).

- The remuneration proxy (cap) on employee loans for immovable property will be increased from R250 000 to R360 000 (last amended in 2018).

- The market value of property in respect of employee loans for immovable property will be increased from R450 000 to R650 000 (last amended in 2018).

- The maximum compensation exemption for employees dying in fulfilment of duties will be increased from R300 000 to R800 000 (last amended in 2007).

- The maximum exemption for awards for bravery and long service will be increased from R5 000 to R16 000 (last amended in 2017).

Capital gains tax:

- The capital gains tax exemption on the sale of a small business for older persons is increased from R1.8 million to R2.7 million. This applies to small businesses worth R15 million instead of the R10 million previously. Both previously increased in 2012.

- The capital gains tax exclusion at death is increased from R300 000 to R440 000 (previously increased in 2012).

- The capital gains tax exclusion in respect of the disposal of a primary residence is increased from R2 million to R3 million (previously increased in 2012).

- The annual capital gains tax exclusion is increased from R40 000 to R50 000 (previously increased in 2017).