South African companies that expand into Africa, mostly set up subsidiaries in the target country for various reasons. However, the financing options to optimise the after-tax returns on the investment then become important as companies are often set up with nominal share capital and funded through inter-company loans.

It is imperative that a number of strategic issues need to be considered from a tax and regulatory perspective early on in the process. For example, it needs to be established whether the South African company has an offshore parent. Should this be the case, then it is unlikely that South Africa will be used as an intermediate holding company jurisdiction as the parent company may be subject to Controlled Foreign Company legislation (CFC), similar to South Africa, so most multinationals avoid multiple-layered CFC regimes and invest directly from the holding structure. Many funding decisions involve the treasury area and most have tax consequences that should be considered.

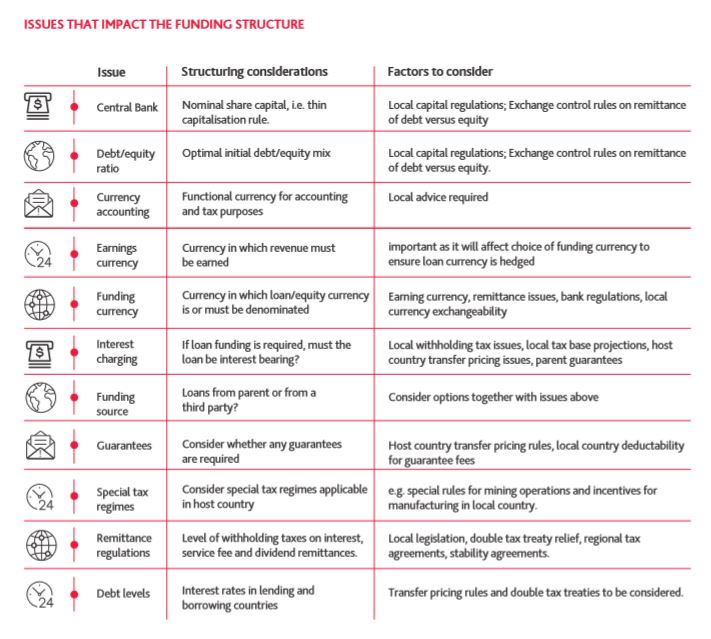

Issues that impact the funding structure of a locally domiciled investor without a foreign controlling shareholder: